The Numbers Don’t Lie: Record-Breaking Inequality in 2024

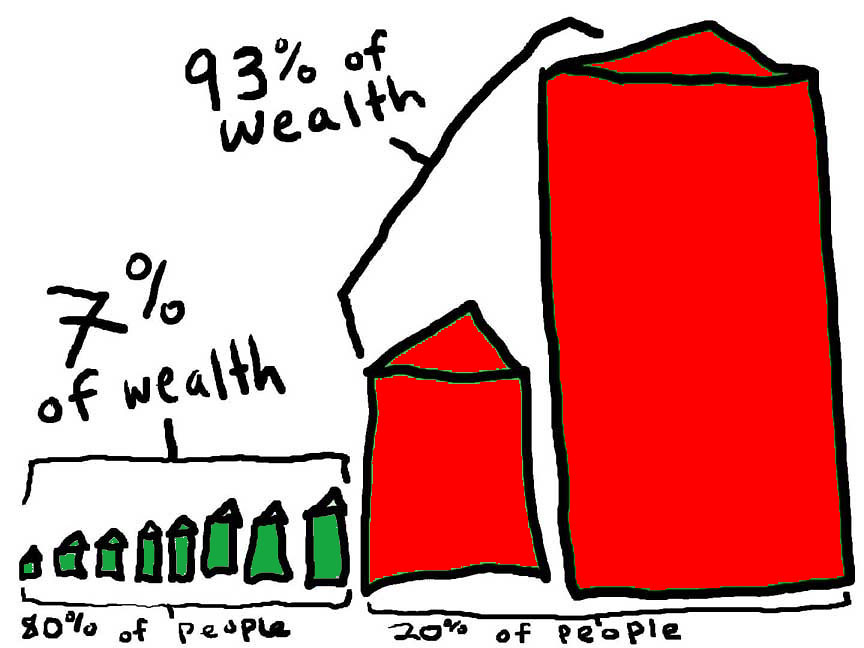

The top 1% of Americans now control more than 32% of all U.S. wealth, according to Federal Reserve data from 2024. This represents the highest concentration of wealth since the 1920s, just before the Great Depression. Meanwhile, the bottom 50% of Americans hold just 2% of total wealth, a figure that has remained virtually unchanged for decades. What’s particularly shocking is that this gap accelerated during the pandemic, with billionaires adding $2.4 trillion to their net worth while millions of working families struggled to pay rent. The Oxfam report from early 2024 revealed that the richest 1% accumulated nearly twice as much wealth as the rest of the world combined over the past two years.

Technology Creates Winners and Losers at Lightning Speed

Silicon Valley’s tech boom has minted more millionaires and billionaires than any industry in history, but it’s also eliminated millions of middle-class jobs. A 2023 MIT study found that artificial intelligence and automation have displaced over 400,000 manufacturing jobs in the past five years alone. Companies like Amazon and Tesla have seen their founders become the world’s richest people while simultaneously reducing their workforce through robotics and AI. The irony is stark: the same technologies that make companies incredibly profitable are the ones putting their customers out of work. This creates a feedback loop where fewer people can afford the products these efficient companies produce, yet the owners get richer from reduced labor costs.

Real Estate Has Become the Ultimate Wealth Divider

Homeownership rates among young adults have plummeted to historic lows, with only 43% of millennials owning homes compared to 51% of Gen X at the same age. Property values have increased 89% since 2020 in major metropolitan areas, according to the National Association of Realtors’ 2024 report. Those who already owned property before this surge have seen their net worth skyrocket, while renters face monthly payments that often exceed what mortgage payments would be. Private equity firms have purchased over 300,000 single-family homes since 2020, converting potential homeowners into permanent renters. This shift means wealth that used to build slowly through homeownership now flows directly to investors who can afford to buy properties with cash.

Education Costs Are Crushing the Middle Class Dream

Student loan debt reached a staggering $1.75 trillion in 2024, with the average graduate owing $37,000 upon completion of their degree. What’s particularly devastating is that college costs have increased 1,200% since 1980, while wages have only grown 213% in the same period. Many families are forced to choose between taking on crushing debt or watching their children fall behind in an increasingly competitive job market. The Federal Reserve’s 2024 survey showed that 43% of recent graduates live with their parents because they can’t afford both student loan payments and housing costs. Meanwhile, wealthy families can pay for their children’s education outright, giving them a debt-free start in life that compounds into massive advantages over time.

Stock Market Gains Favor Those Who Already Have Money

While the S&P 500 has delivered impressive returns over the past decade, 84% of all stock market wealth is owned by the top 10% of earners, according to 2024 Federal Reserve data. The bottom 50% of Americans own virtually no stocks at all, missing out entirely on market gains that have averaged 12% annually since 2020. Even when middle-class families do invest, they typically have much smaller amounts at risk, meaning a 20% market gain might add $2,000 to their portfolio while adding $200,000 for wealthy investors. The psychological barriers are equally important: people living paycheck to paycheck can’t afford to risk their emergency funds in volatile markets. This creates a situation where economic growth primarily benefits those who least need additional wealth.

Healthcare Costs Create Financial Catastrophes for Regular Families

Medical bankruptcies affect approximately 530,000 American families annually, with 68% of those families having health insurance at the time of their illness, according to a 2023 American Journal of Public Health study. The average cost of a three-day hospital stay now exceeds $30,000, while a cancer diagnosis can easily result in six-figure medical bills even with insurance coverage. Wealthy families can afford concierge medicine, preventive care, and the best specialists, helping them avoid both health problems and financial ruin. Working-class families often delay necessary medical care, leading to more expensive emergency treatments later. The cruel irony is that health problems often prevent people from working, creating a downward spiral where medical debt destroys both health and wealth simultaneously.

Small Businesses Face Corporate Competition They Can’t Match

Amazon’s market dominance has contributed to the closure of over 100,000 small retail businesses since 2020, according to the Small Business Administration’s 2024 report. Large corporations can operate at losses for years to drive out competition, then raise prices once they’ve achieved market dominance. They also have access to cheap capital through corporate bonds and bank loans that small business owners simply cannot obtain. During the pandemic, many small businesses permanently closed while large corporations received billions in federal aid and saw their stock prices soar. The result is that business ownership, once a reliable path to middle-class wealth, has become increasingly difficult for ordinary entrepreneurs to achieve.

Tax Laws Written by and for the Wealthy

The effective tax rate for billionaires is approximately 8.2%, while middle-class families typically pay between 22-24% of their income in federal taxes, according to a 2024 White House analysis. Wealthy individuals can use sophisticated tax strategies like charitable remainder trusts, family limited partnerships, and offshore accounts that are unavailable to regular taxpayers. Capital gains are taxed at much lower rates than wages, meaning people who live off investment returns pay less than those who work for their money. The carried interest loophole alone saves hedge fund managers billions annually, while teachers and nurses pay higher effective rates on their salaries. Recent attempts at tax reform have been consistently blocked by lobbying efforts funded by the same ultra-wealthy individuals who benefit from current policies.

Inheritance Laws Perpetuate Generational Advantages

Only estates worth more than $12.92 million face federal estate taxes in 2024, meaning 99.8% of inheritances pass tax-free to the next generation. Wealthy families use dynasty trusts and other legal structures to pass billions to their descendants while minimizing tax obligations. The average inheritance among the top 1% is over $4 million, while typical American families leave less than $70,000 to their children, often in the form of a modest home with an outstanding mortgage. Studies show that inherited wealth compounds much faster than earned wealth because it can be invested immediately rather than spent on living expenses. This creates a permanent aristocratic class where financial success depends more on family background than individual effort or talent.

Geographic Mobility Has Become a Luxury

Moving to areas with better job opportunities now requires upfront costs that many families simply cannot afford, with average relocation expenses exceeding $15,000 according to 2024 moving industry data. High-paying jobs are increasingly concentrated in expensive metropolitan areas like San Francisco, New York, and Seattle, where housing costs consume 50-70% of median incomes. Wealthy individuals can easily relocate for opportunities, buy homes in multiple markets, or work remotely from low-cost areas while earning high-cost-area salaries. Working-class families become trapped in declining regions with limited economic prospects because they lack the financial resources to move elsewhere. This geographic sorting creates a vicious cycle where opportunity clusters in places that are increasingly unaffordable for the people who need those opportunities most.

Start Investing Early, Even with Small Amounts

The power of compound interest becomes dramatically clear when you start investing in your twenties versus your thirties. A person who invests $200 monthly starting at age 25 will have over $1.3 million by retirement, while someone who waits until 35 and invests the same amount will only accumulate $615,000. Low-cost index funds through platforms like Vanguard or Fidelity allow you to start with as little as $100 and avoid the high fees that eat into returns. Apps like Acorns or Stash can automatically invest your spare change, making it painless to build wealth gradually. The key is consistency rather than large amounts – investing $50 monthly for decades beats investing $5,000 once and then stopping.

Learn High-Value Skills That AI Can’t Replace

Focus on developing skills that require human creativity, emotional intelligence, or complex problem-solving that automation cannot replicate. Trades like plumbing, electrical work, and HVAC repair are experiencing massive labor shortages and offer six-figure earning potential without requiring college degrees. Digital marketing, data analysis, and cybersecurity skills are in extremely high demand and can be learned through online courses that cost less than one semester of college. Healthcare professions, particularly nursing and physical therapy, offer stable employment and growth opportunities as the population ages. The goal is to position yourself in industries where human skills remain essential, giving you leverage to demand higher wages as automation eliminates other jobs.

Buy Assets Instead of Liabilities

Rich people buy things that put money in their pockets, while poor people buy things that take money out of their pockets. A rental property, dividend-paying stocks, or a small business generates ongoing income, while a luxury car or expensive gadgets only drain your finances through depreciation and maintenance costs. Consider house hacking, where you buy a duplex, live in one unit, and rent out the other to cover your mortgage payments. Even small assets like a food truck, online course, or rental equipment can provide additional income streams that compound over time. The mindset shift from consumer to investor is perhaps the most important change you can make in building long-term wealth.

Negotiate Everything and Understand Your Worth

Most people leave thousands of dollars on the table annually by failing to negotiate salaries, bills, and major purchases. Research shows that employees who negotiate their starting salary earn over $600,000 more during their careers than those who accept initial offers. You can often reduce monthly bills by 10-20% simply by calling providers and asking for discounts or threatening to switch to competitors. Freelancers and contractors should regularly raise their rates as their skills improve – the worst clients to say is no, and better clients will happily pay for quality work. Keep detailed records of your accomplishments and contributions at work to build a compelling case for raises and promotions during performance reviews.

Build Multiple Income Streams Like the Wealthy Do

Millionaires typically have seven different income sources, while most people rely entirely on a single paycheck that can disappear at any moment. Side hustles like driving for rideshare services, selling items online, or freelance consulting can provide additional cash flow and financial security. Passive income through dividend stocks, rental properties, or royalties from creative work can eventually replace your day job entirely. The internet has created countless opportunities to monetize skills and knowledge through online courses, YouTube channels, affiliate marketing, and digital products. Start small with one additional income stream, then gradually build others as your first ventures become profitable and sustainable.

What strikes me most about wealth inequality is how it feeds on itself – the rich get richer not because they’re necessarily smarter or work harder, but because they have access to wealth-building tools that others don’t. But here’s the thing: many of these tools are more accessible today than ever before, if you know where to look and have the discipline to use them consistently. The question isn’t whether you can compete with billionaires, but whether you can build enough wealth to secure your own future and break the cycle for your family. What’s stopping you from starting today?