Savings accounts have long been the go-to option for those looking to store their money safely. But with traditional savings accounts offering modest interest rates—often averaging around 0.42%—many are exploring alternative investment options that promise higher returns. In this article, we delve into ten such alternatives, comparing their potential benefits and risks to help you make informed financial decisions.

High-Yield Savings Accounts

High-yield savings accounts function much like traditional savings accounts but offer significantly higher interest rates. These accounts are typically provided by online banks, which can afford to offer better rates due to their lower overhead costs. For example, some online banks offer annual percentage yields (APYs) exceeding 4%, a stark contrast to the national average of 0.42% for standard savings accounts. While these accounts are FDIC-insured and offer easy access to funds, it’s crucial to keep an eye on interest rate fluctuations, as they can change based on market conditions. They are a viable option for those seeking higher interest without sacrificing security.

Certificates of Deposit (CDs)

Certificates of Deposit are time-bound deposits that promise a fixed interest rate over a specified term, ranging from a few months to several years. In return for locking in your funds for the term’s duration, banks usually offer higher interest rates than regular savings accounts. As of October 2023, average CD rates varied from 4.60% to 5.55%, depending on the term length. However, accessing these funds before maturity can lead to penalties, making CDs less liquid than other options. They are ideal for individuals who can afford to set aside money for a fixed period without needing immediate access.

Money Market Accounts (MMAs)

Money Market Accounts blend features of savings and checking accounts, often providing higher interest rates along with limited check-writing and debit card privileges. These accounts are FDIC-insured up to applicable limits, offering a secure investment avenue. However, they might require higher minimum balances and can impose restrictions on the number of transactions per month. It’s also important to note that while the interest rates can be competitive, they can fluctuate with market conditions. MMAs are excellent for those who want a mix of liquidity and higher returns.

Peer-to-Peer (P2P) Lending

Peer-to-Peer lending platforms connect investors directly with borrowers, allowing individuals to lend money in exchange for interest payments. This investment avenue can yield higher returns compared to traditional savings accounts, with some platforms offering average annual returns between 5% to 8%. However, P2P lending carries heightened risk, including the potential for borrower default, and lacks FDIC insurance. Diversifying loans across multiple borrowers can help mitigate some of this risk. It’s a compelling option for those willing to take on more risk for the chance of higher returns.

Treasury Securities

U.S. Treasury securities, including bonds, bills, and notes, are government-backed investments considered low-risk. They offer various maturities and interest rates, with longer-term securities typically providing higher yields. For example, 10-year Treasury bonds have historically offered yields around 2% to 3%. These securities are exempt from state and local taxes, enhancing their appeal to certain investors. However, they may offer lower returns compared to other investment options and can be subject to interest rate risk. They are suitable for risk-averse investors seeking stability.

Real Estate Investments

Investing in real estate can provide rental income and potential property value appreciation. Historically, real estate investments have yielded average annual returns between 4% to 7%. Options include purchasing physical properties or investing in Real Estate Investment Trusts (REITs), which allow for real estate investment without the need to manage properties directly. While real estate can diversify an investment portfolio, it requires significant capital and involves risks such as market volatility and property management challenges. It’s a tangible investment with potential for long-term growth.

Mutual Funds

Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other securities. Managed by professional fund managers, they can offer average annual returns ranging from 5% to 8%, depending on the fund’s investment strategy. While mutual funds provide diversification and professional management, they are subject to market risks, and returns are not guaranteed. Additionally, management fees can impact overall returns. Mutual funds are suitable for those seeking a hands-off investment approach with potential for growth.

Exchange-Traded Funds (ETFs)

ETFs are similar to mutual funds but trade on stock exchanges like individual stocks. They offer diversification across various asset classes and sectors and typically have lower expense ratios compared to mutual funds. ETFs can be an efficient way to invest in specific markets or strategies but are subject to market volatility, and their value can fluctuate throughout the trading day. They are ideal for investors looking for flexibility and lower costs.

Cryptocurrencies

Cryptocurrencies are digital or virtual currencies that use cryptography for security. They have gained popularity as alternative investments due to their potential for high returns. However, cryptocurrencies are highly volatile and can experience significant price swings. For instance, Bitcoin has seen substantial fluctuations in value over short periods. Investing in cryptocurrencies carries a high risk, and it’s crucial to conduct thorough research and consider your risk tolerance before investing. They are a modern, speculative investment with potential for high reward.

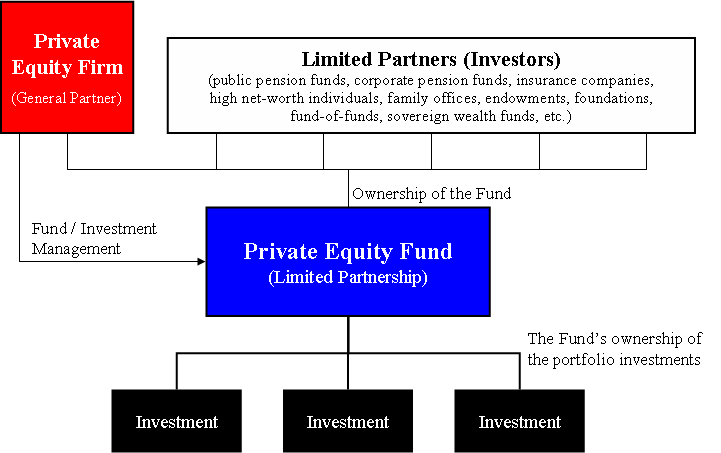

Private Equity

Private equity involves investing directly in private companies or buyouts of public companies, resulting in their delisting from public stock exchanges. Over the 20-year period ending in 2022, private equity investments achieved average annual returns of 14.75%, outperforming the S&P 500’s 9.25% return. However, private equity investments are typically illiquid, require substantial capital, and are often accessible only to accredited investors. They also involve higher risk due to the potential for business failures. They are suitable for those with significant capital and a high-risk tolerance.

While traditional savings accounts offer security and liquidity, their low-interest rates may not meet the financial goals of all investors. Exploring alternative investments can provide opportunities for higher returns, but it’s essential to consider factors such as risk tolerance, investment horizon, and liquidity needs. Diversifying your investment portfolio across different asset classes can help balance potential risks.